Since the number of articles dealing with models related to portfolio creation has increased, I will make it into a link collection. (I will add links as needed)

Models for Asset Allocation (Models for deciding portfolio proportions)

The following models model how to decide portfolio proportions using expected returns etc. on the premise that such information is known or calculated.

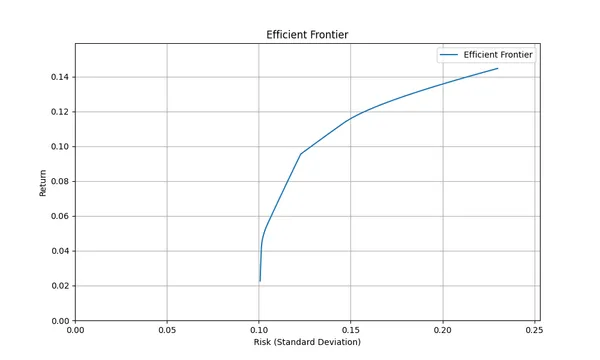

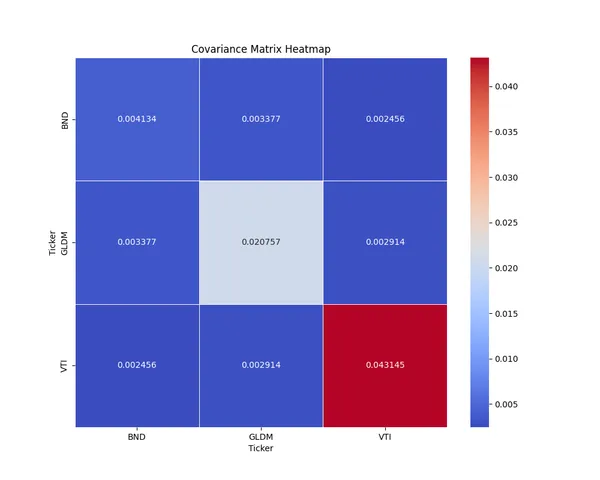

Mean-Variance Optimization

Pythonで学ぶモダンポートフォリオ理論:平均分散最適化の考え方

>-

Pythonで解くモダンポートフォリオ理論:平均分散最適化と効率的フロンティアの計算法

>-

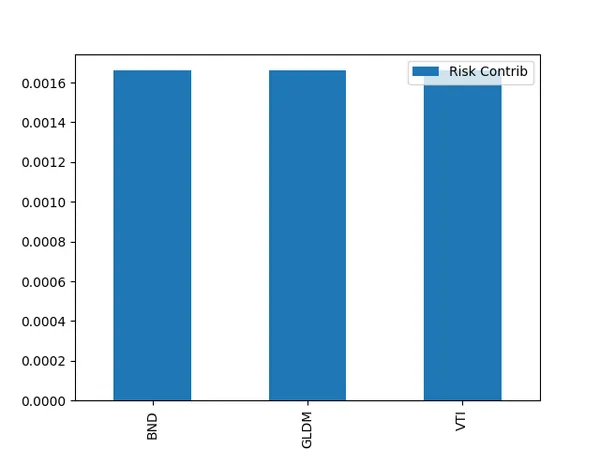

Risk Parity Portfolio

リスクパリティポートフォリオ徹底解説:基本概念、計算式からPython実装まで

>-

Models for Calculating Expected Returns

The following are models for calculating expected returns. You can operate by using the expected returns calculated with these and plugging them into the portfolio proportion decision models introduced above.

CAPM

投資リスクを管理するためのCAPM入門:メリットとデメリットを詳しく解説

>-

Black-Litterman Model

ブラック・リッターマン法による投資ポートフォリオ最適化: 基本概念とPythonでの実践

>-

Fama-French 3-Factor Model

Fama-French 3ファクターモデルの基本とPython実装

>-

Barra Model

投資リスクを評価する「Barraモデル」とは?マルチファクターモデルの仕組みと計算方法を解説

>-

Models for Risk Management

VaR, CVaR

Backtraderを使った簡単バックテスト:Buy and Hold戦略編

>-

Others

I will introduce terms used as concepts in the above models.

Market Portfolio

マーケットポートフォリオの基本と計算方法:投資リスクを減らす秘訣

>-