Finance & Markets

3 min read

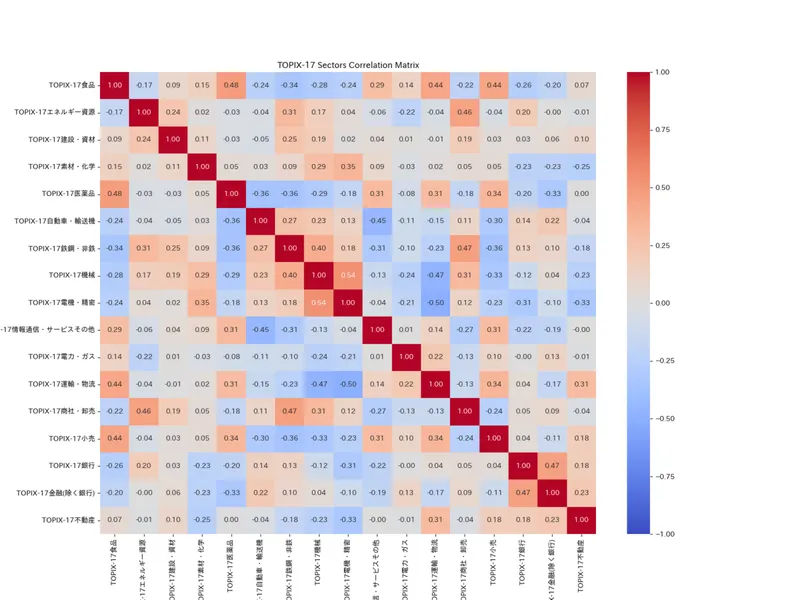

Portfolio Diversification: Sector Correlation Analysis in Python

Explore sector analysis using correlation coefficients and Python. Includes practical concepts and results calculated from actual market data.

7 articles

Explore sector analysis using correlation coefficients and Python. Includes practical concepts and results calculated from actual market data.

Master the Fama-French 3-Factor Model with our Python guide. Learn how market, size, and value factors drive investment returns.

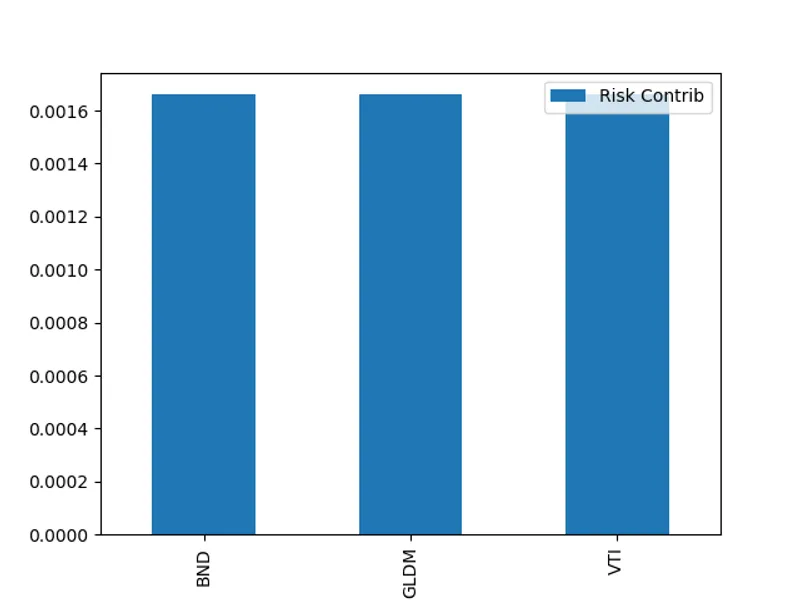

In this article, explaining basic concept, Merit, calculation method of Risk Parity Portfolio, and implementation method in Python.

Optimize asset allocation using the Black-Litterman Model. Learn to blend market data with investor views using Python and Bayesian approaches.

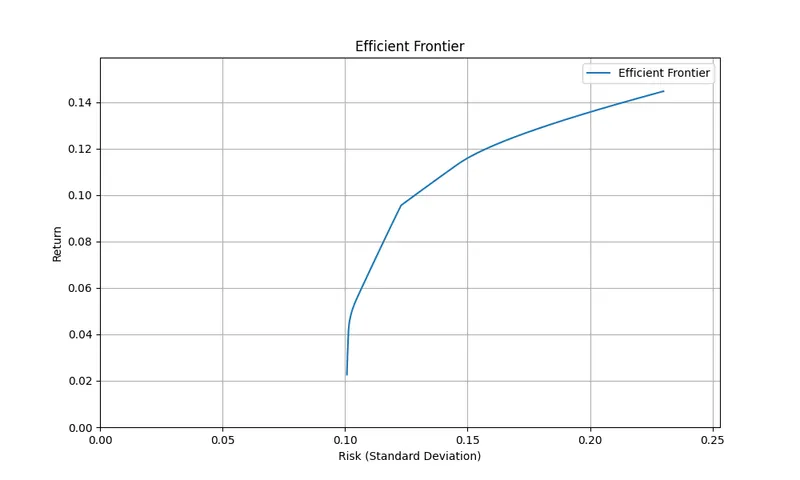

Calculate Mean-Variance Optimization and Efficient Frontiers using Python. A detailed guide covering theory and practical implementation for portfolios.

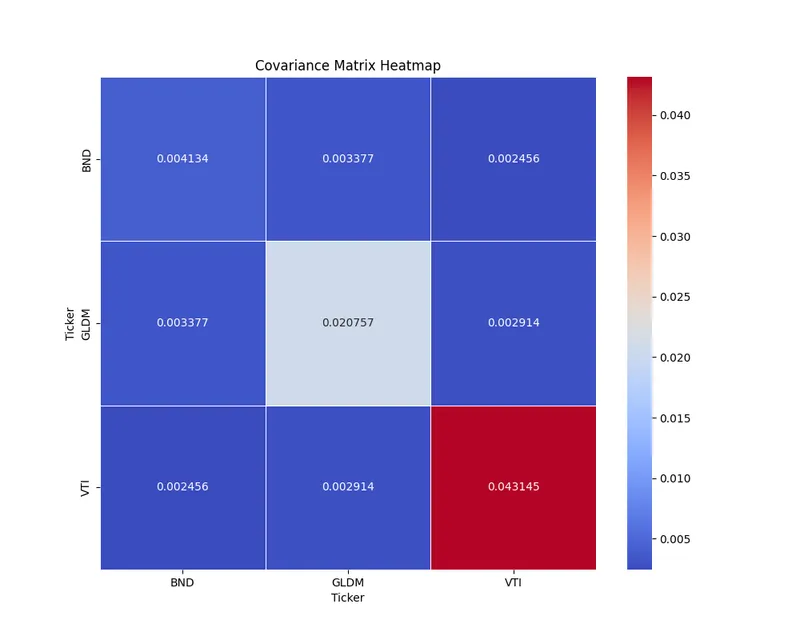

Construct optimal portfolios using Python. A step-by-step guide to calculating returns, risk, covariance, and building the Efficient Frontier.

Master the Capital Asset Pricing Model (CAPM). Learn basic concepts, calculation steps, and Python implementation with yfinance for modeling.