Barra model playing important role in investment and risk management is a powerful tool to evaluate risk of portfolio using multiple factors and predict return. In this article, briefly explaining basic mechanism of Barra model and its actual calculation method.

Overview of Barra Model

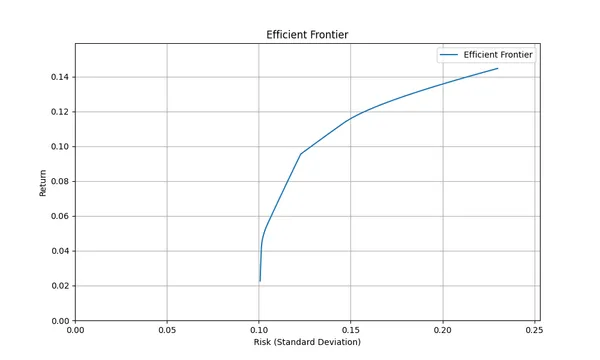

Barra model is a multi-factor model for risk management and asset management, mainly used to evaluate risk of portfolio and predict return. Particularly characteristic point of this model is that customization such as adding or subtracting factors to use is possible depending on case.

In terms of practical use, it is used by investors and financial institutions to evaluate risk/return characteristics of portfolio and perform appropriate risk adjustment. Also it is useful as a tool to decompose investment performance at factor level and clarify what contributed to performance.

Calculation Method of Barra Model

Calculation method itself is relatively simple and can be expressed only by formula below (I think obtaining beta is tough part rather).

Difference with CAPM, Fama-French 3 Factor Model

If you look at formula you might understand, but it is like a relative of formulas of CAPM and Fama-French 3 Factor Model. But there is one different point. Risk-free rate is not considered. Please be careful about this point only when calculating.

This is because barra model is not for calculating return, but for measuring how much which factor influences return. Since it is for evaluating relative risk, risk-free rate is not used. However, it doesn’t mean there is problem if considered, and it is thought calculation emphasizing return more is possible if considered.

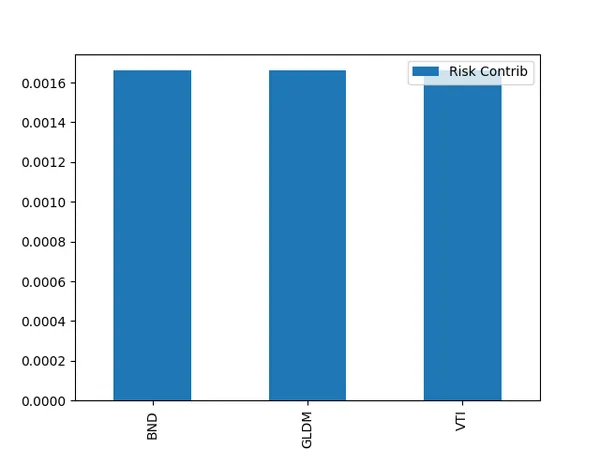

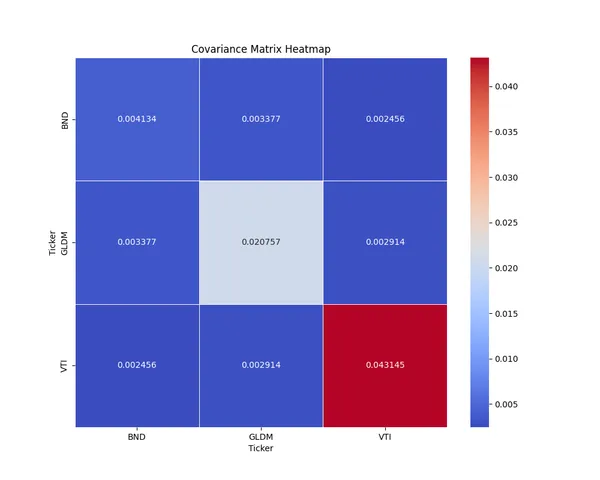

Calculation Method of Beta

To calculate beta, step on following procedure.

- Data Collection

- Collect return data of assets and return data of factors used in model. This includes past return data of each factor.

- Perform Regression Analysis

- Perform regression analysis of asset return against factor return. In this case, use asset return as dependent variable and return of each factor as independent variable.

- Extraction of Beta

- Extract regression coefficient for each factor from result of regression analysis as beta. This regression coefficient shows how sensitive asset return is to factor return.

Note: Factor return means return linked to specific factor.

How to acquire factor return data

Reading calculation method of beta, I wonder how to acquire factor return, but usually it is not circulating. Basically it is necessary to buy or calculate by yourself. There are 3 acquisition methods including finding it luckily sometimes.

- Use of Data Provider

- Access API or database of data provider and download necessary factor return data. (Mostly costs money)

- Bloomberg, MSCI etc.

- Use of Public Data

- Sometimes publicly available for research purpose. One used in article of Fama-French is an example.

-

Fama-French 3ファクターモデルの基本とPython実装

>-

- Other Data Sets might have it too

- Data Collection by yourself

- It is also possible to use index as factor as is, or calculate factor return yourself from market data

Case of calculating beta with Python

Explaining briefly in article below. For simplicity doing with one factor, but doing this with multiple factors is barra model.

>-

Conclusion

Through this article, I think you could understand basic part of Barra model. I hope this information helps improvement of your investment judgment and risk management.

If you want to know other models related to portfolio construction, please utilize the link collection below.

投資ポートフォリオ構築に関するモデル記事のリンク集。資産配分・期待リターン計算・リスク管理モデルを体系的にまとめています。