Advantages of Market Portfolio

| Feature | Description |

|---|---|

| Diversification Effect | Since Market Portfolio includes extremely broad assets, risk diversification effect is minimized. Can reduce overall risk without depending on risk of specific asset class or individual stock. |

| Market Benchmark | Since Market Portfolio theoretically reflects whole market, it is used as benchmark when evaluating performance of other portfolios or investment strategies. This allows investors to evaluate how much performance their investment is raising against whole market. |

| Basis of Efficient Market Hypothesis | Based on Efficient Market Hypothesis (EMH), Market Portfolio is considered most efficient portfolio, having most excellent balance of risk and return. According to this hypothesis, investing in Market Portfolio becomes optimal strategy. |

| Standard for Asset Allocation | Market Portfolio is used as standard for asset allocation, helping construction of long-term investment strategy. This makes it easier for investors to maintain balanced portfolio. |

Calculation Method

1. List up Assets

List up all investable asset classes.

2. Calculation of Market Value

Calculate market value of each asset class.

3. Calculation of Total Market Value

Sum market value of all identified assets to find total market value of portfolio.

4. Calculation of Asset Weight

Weight of each asset in Market Portfolio is calculated as follows:

Here,

- is weight of asset .

- is market value of asset .

- is total market value of all assets in portfolio.

5. Calculate Expected Return of Market Portfolio

Expected return of Market Portfolio can be calculated using weighted average of expected return of each asset:

Here,

- is expected return of portfolio.

- is weight of asset .

- is expected return of asset .

- is total number of assets in portfolio.

6. Calculate Risk of Market Portfolio

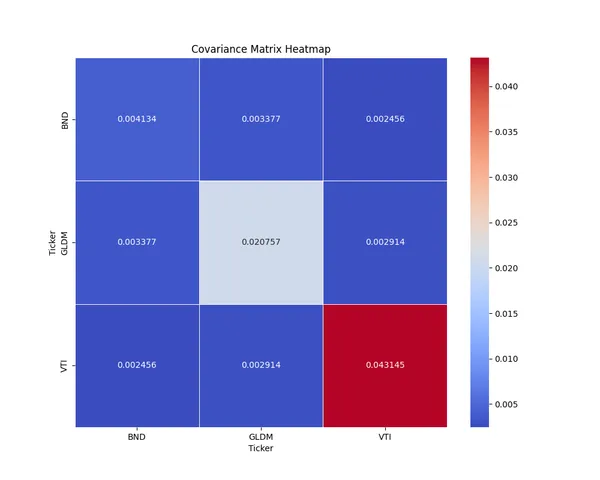

Risk of Portfolio (Standard Deviation) can be calculated using Covariance Matrix of asset returns:

Here,

is total number of assets in portfolio.

is variance of portfolio.

is weight of asset .

is weight of asset .

is covariance of asset and asset .

Calculation Example

1. List up Assets

Asset classes are assumed as below following general Robo-advisor.

- US Stock

- Developed Stock (Excluding US)

- Emerging Stock

- US Bond

- High Yield Bond

- Emerging Bond

- US Real Estate

- Gold

2. Calculation of Market Value

This time I had ChatGpt bring plausible data. (Leaving accuracy aside)

- US Stock: Approx. 50.8 Trillion USD

- Developed Stock (Excluding US): Approx. 27.6 Trillion USD

- Emerging Stock: Approx. 10.2 Trillion USD

- US Bond: Approx. 23.2 Trillion USD

- High Yield Bond: Approx. 1.7 Trillion USD

- Emerging Bond: Approx. 3.2 Trillion USD

- US Real Estate: Approx. 11.5 Trillion USD

- Gold: Approx. 1.3 Trillion USD

3. Calculation of Total Market Value

Total Market Value = Approx. 129.5 Trillion USD

4. Calculation of Asset Weight

This becomes ratio of Market Portfolio.

| Asset Class | Market Value (Trillion USD) | Weight |

|---|---|---|

| US Stock | 50.8 | 0.3923 |

| Developed Stock (Excluding US) | 27.6 | 0.2131 |

| Emerging Stock | 10.2 | 0.0788 |

| US Bond | 23.2 | 0.1792 |

| High Yield Bond | 1.7 | 0.0131 |

| Emerging Bond | 3.2 | 0.0247 |

| US Real Estate | 11.5 | 0.0888 |

| Gold | 1.3 | 0.0100 |

Conclusion

Market Portfolio is very convenient as base portfolio to disperse investment risk and perform efficient asset allocation. Except when you want to make portfolio by yourself or evaluate, chance to need calculation might not exist much, but since it’s a word appearing often in theory, I think there is no loss remembering.