Backtrader is powerful library facilitating backtest in Python. In this article, I explain method to implement Rebalance and perform backtest using data of past 10 years simply.

1. Preparation of Environment

Installation of library

# install requirement%pip install backtrader yfinance matplotlib2. Import of Library

Import necessary libraries

# import libsimport datetimeimport backtrader as btimport yfinance as yfimport matplotlib.pyplot as plt3. Parameter Setting

Set necessary parameters.

## ticker and ratioTICKERS = {"VTI": 0.4, "BND": 0.4, "GLD": 0.2}## start date and end dateFROMDATE = datetime.datetime(2014, 7, 1)TODATE = datetime.datetime(2024, 7, 1)4. Implement Strategy

Strategy - Backtrader

python backtesting trading algotrading algorithmic quant quantitative analysis

www.backtrader.com

# Implement strategy of rebalanceclass RebalanceOncePerMonth(bt.Strategy): def __init__(self): self.last_rebalance = None # Date last rebalanced def next(self): dt = self.datetime.date() if self.last_rebalance is None or (dt - self.last_rebalance).days >= 30: # If 30 days or more passed # self.broker.add_cash(1000) # In case of accumulation, do add_cash every certain period self.rebalance_portfolio() self.last_rebalance = dt def rebalance_portfolio(self): total_value = self.broker.getvalue() for data in self.datas: ticker = data._name allocation = data.target target_value = total_value * allocation current_value = self.getposition(data).size * data.close[0] difference = target_value - current_value if difference > 0: # Buy size = difference // data.close[0] self.buy(data=data, size=size) elif difference < 0: # Sell size = -difference // data.close[0] self.sell(data=data, size=size)5. Execute Backtest

Perform data reading, and execute backtest.

# Initialization of backtradercerebro = bt.Cerebro()cerebro.broker.set_cash(10000)cerebro.addstrategy(RebalanceOncePerMonth)# Read data from yahoofinancefor ticker, target in TICKERS.items(): data = bt.feeds.PandasData( dataname=yf.download(ticker, start=FROMDATE, end=TODATE) ) data.target = target cerebro.adddata(data, name=ticker)# Execution of backtestprint('Starting Portfolio Value: %.2f' % cerebro.broker.getvalue())cerebro.run()print('Final Portfolio Value: %.2f' % cerebro.broker.getvalue())Starting Portfolio Value: 10000.00Final Portfolio Value: 13314.386. Visualize result of backtest

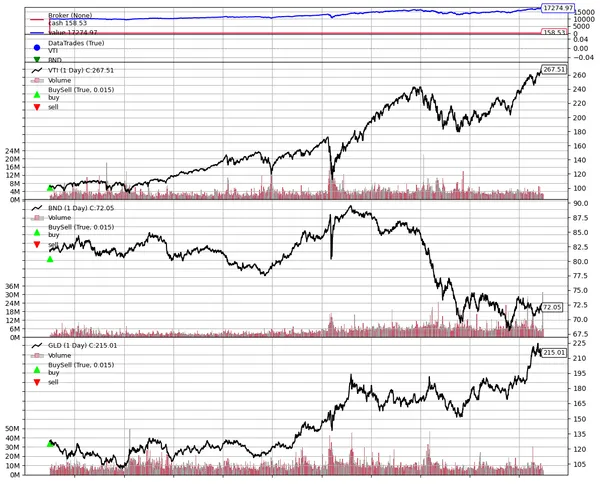

It can be seen that Buy and Sell are performed appropriately.

plt.rcParams['figure.figsize'] = [12, 10]cerebro.plot(iplot=False)